You ran the numbers on the funeral home you want to buy. Revenue looks solid, margins are healthy, and the seller seems motivated. Then your insurance broker pulls the experience modification rate — 1.38. Your annual workers’ comp premium just jumped 38% above the industry baseline, and that number follows the business for at least three years. Nobody mentioned it during the first two months of due diligence.

Why Workers’ Comp Is a Bigger Variable Than You Think

Funeral homes are not office buildings. They are not retail stores. They are facilities where employees handle hazardous chemicals, lift heavy objects (including human remains that can weigh 300 pounds or more), drive commercial vehicles in all conditions, and interact with biohazardous materials daily. Workers’ compensation insurance reflects that risk profile — and the premium range across funeral homes is enormous.

A small, well-run funeral home with 200 cases per year and a clean claims history might pay $15,000 annually for workers’ comp. A larger operation with 600 cases, a fleet of vehicles, and a history of claims can pay $60,000 or more. The difference between those two numbers is not just size — it is the experience modification rate.

NCCI Classification Codes for Funeral Homes

The National Council on Compensation Insurance (NCCI) assigns classification codes that determine your base premium rate. Funeral homes typically involve three codes:

- Code 7720 — Undertakers/Funeral Directors: Covers embalming, body preparation, arrangement conferences, and funeral service conduct. This is the primary code and carries the highest base rate because of chemical exposure and physical handling risks.

- Code 8810 — Clerical/Office: Covers administrative staff who do not handle remains or perform physical funeral home tasks. Lowest rate.

- Code 7380 — Drivers: Covers removal drivers, hearse operators, and anyone whose primary function involves operating funeral home vehicles. Elevated rate due to vehicle accident exposure.

Your premium is calculated by applying each code’s rate to the payroll allocated to that classification, then multiplying the total by your experience modification rate. Getting the payroll allocation right matters — misallocating a funeral director’s salary to the clerical code is a compliance violation that can trigger an audit premium adjustment.

The Experience Modification Rate: What It Is and Why It Transfers

The EMR is a multiplier that adjusts your workers’ comp premium based on the business’s actual claims history compared to the expected claims for businesses of similar size and type. It is the single most impactful variable in your workers’ comp cost structure.

How EMR Works

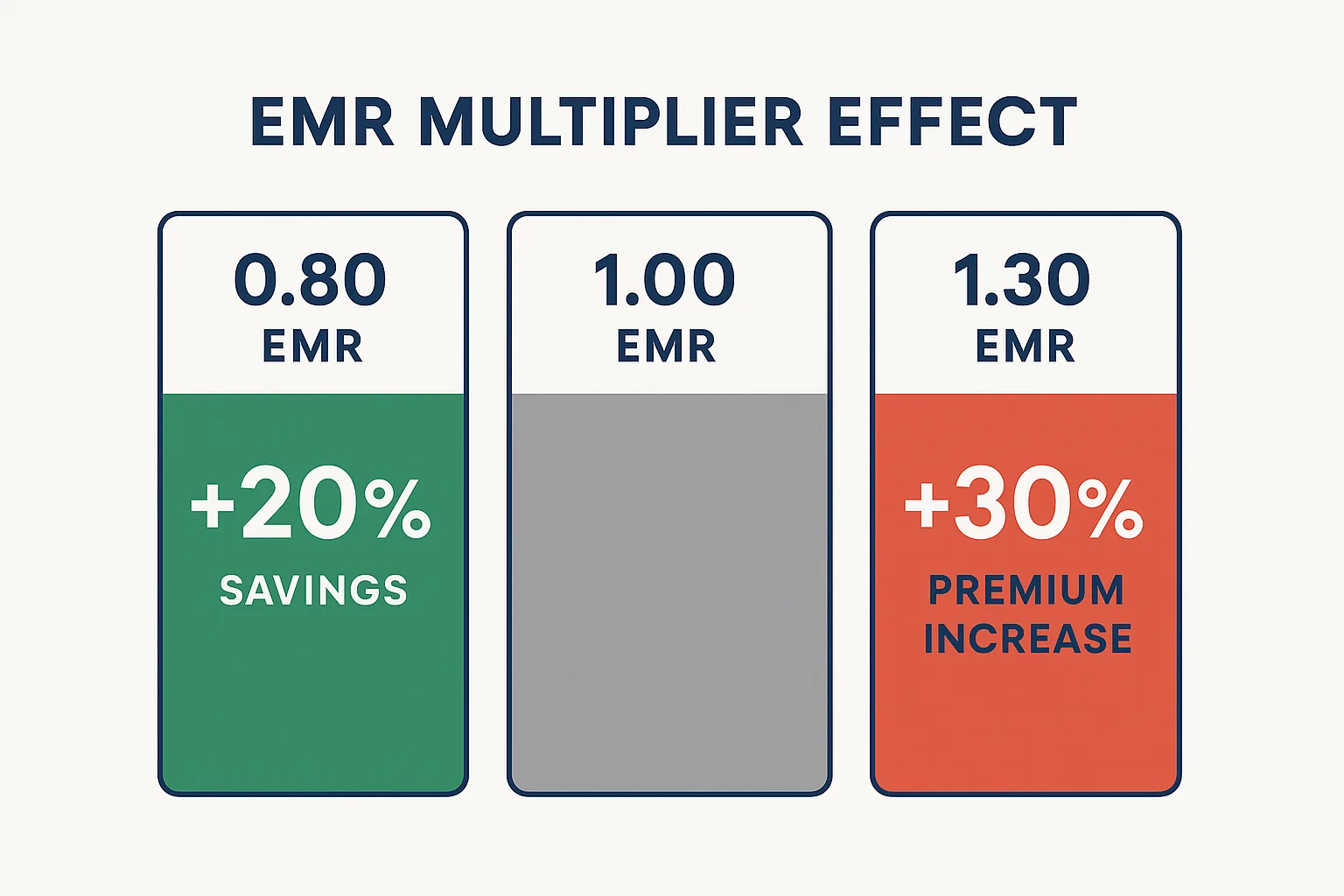

- 1.0 = industry average. Your claims history matches what NCCI expects for a funeral home of your size.

- Below 1.0 = better than average. Fewer or smaller claims than expected. A 0.85 EMR means your premium is 15% below baseline.

- Above 1.0 = worse than average. More or larger claims than expected. A 1.35 EMR means your premium is 35% above baseline.

The calculation uses a three-year claims window, excluding the most recent policy year (because those claims are still developing). NCCI compares the funeral home’s actual losses against expected losses for its classification and payroll size, with adjustments for claim frequency versus severity. Frequency — multiple smaller claims — is weighted more heavily than a single large claim, because frequent claims suggest systemic safety problems.

The Transfer Problem

Here is the critical point for buyers: the EMR follows the Federal Employer Identification Number (FEIN), not the individual owner.

In a stock purchase or membership interest purchase, you acquire the existing entity and its FEIN. The EMR transfers with the entity. There is no reset, no appeal, no fresh start. Whatever claims history that entity accumulated over the past three-plus years is now driving your premium.

In an asset purchase, the outcome depends on your state and how you structure the new entity. If you obtain a new FEIN and establish a genuinely new entity with no continuity of operations (different entity, different ownership, different management), some states will assign you a 1.0 EMR as a new business. But most states have combination rules — if you acquire the assets, retain the employees, and continue the same operations at the same location, the state rating bureau will likely transfer the prior entity’s EMR to your new entity. The NCCI Experience Rating Plan Manual details these combination and successor rules.

Do not assume you can escape a bad EMR by creating a new LLC. The rating bureaus have seen that approach many times and have rules specifically designed to prevent it.

The Claims That Drive Funeral Home EMR

Understanding what generates claims helps you evaluate the risk profile of the funeral home you are buying — and predict whether the EMR is likely to improve or worsen under your ownership.

Formaldehyde Exposure and Respiratory Claims

Embalming involves daily exposure to formaldehyde, a known carcinogen regulated under OSHA’s Formaldehyde Standard (29 CFR 1910.1048). Respiratory claims from formaldehyde exposure are among the most expensive workers’ comp claims in funeral service because they involve:

- Ongoing medical treatment (not a one-time injury)

- Potential permanent disability ratings

- Long-tail liability (symptoms may develop or worsen over years)

A single formaldehyde-related respiratory claim can generate $50,000–$150,000 in losses and impact the EMR for the full three-year calculation window. During due diligence, check whether the prep room has adequate ventilation, whether the funeral home monitors air quality, and whether it provides proper PPE. Review our OSHA compliance guide for the full evaluation framework.

Lifting Injuries from Removals

Body removal — transporting a decedent from the place of death to the funeral home — is the highest-frequency injury source in funeral service. Staff lift and transfer bodies that may weigh 200–400 pounds from beds, floors, bathtubs, and stairs, often in cramped residential spaces and at unpredictable hours.

Common injuries include:

- Lower back strains and herniated discs

- Shoulder tears (rotator cuff)

- Knee injuries from awkward lifting angles

- Hand and wrist injuries from gurney operation

These claims typically range from $5,000–$40,000 each, but their frequency is what damages the EMR. Three or four lifting claims in a two-year period will push the EMR well above 1.0 even if no single claim is catastrophic.

Vehicle Accidents

Funeral homes operate fleets — first-call vehicles, hearses, flower cars, limousines, and sometimes transport vans. Vehicle accidents produce some of the largest individual claims in funeral service, particularly when a third party is involved.

A hearse involved in a serious accident during a funeral procession can generate six-figure claims. Even minor fender-benders during removals contribute to claims frequency. Evaluate the fleet condition and driver records as part of your workers’ comp risk assessment.

Other Common Claim Sources

- Slip and fall injuries in public areas (chapels, lobbies, parking lots) and work areas (prep rooms with wet floors)

- Needlestick and biohazard exposure during embalming and body preparation

- Repetitive stress injuries from casket handling and display room maintenance

- Assault or emotional trauma claims from volatile family situations (rare but documented)

How to Evaluate Workers’ Comp in Due Diligence

Workers’ comp evaluation requires specific documents and a structured analysis. Here is the process.

Request Five Years of Loss Runs

Loss runs are the detailed claims history reports issued by the funeral home’s workers’ comp insurer. Request five full years, not just three.

Why five years? The EMR calculation uses three years, but you want to see the trajectory. Is claims frequency improving or worsening? Was there a spike three years ago that is about to roll off the calculation? Is there a pattern of claims in a specific department or role?

Each loss run entry shows the claim date, injury type, claimant role, claim status (open or closed), paid amounts, and reserves (amounts the insurer has set aside for future payments on open claims). Open claims with large reserves are particularly important — those reserves are included in the EMR calculation and may be inflated or understated.

Calculate or Verify the EMR

You can request the current EMR from the funeral home’s insurance broker, but verify it independently. Ask your own broker to pull the EMR from NCCI or your state rating bureau. EMRs are public information within the insurance system.

Compare the EMR against the loss runs. If the EMR seems inconsistent with the claims history, there may be data errors, unreported claims, or classification issues that need investigation.

Identify Open Claims and Reserves

Open claims are active liabilities. A funeral home with three open workers’ comp claims, each carrying $20,000 in reserves, has $60,000 in potential future loss development hanging over its EMR.

Ask the seller about the status of every open claim. Is the claimant still receiving treatment? Is there a settlement in progress? Has the claimant returned to work? Open claims that can be settled before closing reduce your inherited EMR impact.

Benchmark Premium to Revenue

For a properly managed funeral home, workers’ comp premium should run approximately 1.5–3% of gross revenue. Calculate this ratio for the target:

- Below 1.5%: Unusually low — verify that all employees are properly covered and that payroll is not being underreported

- 1.5–2.5%: Healthy range for a funeral home with a clean claims history

- 2.5–3.5%: Elevated — likely driven by high EMR, large payroll, or high-risk state

- Above 3.5%: Problematic — investigate claims history and consider the premium impact on your acquisition economics

Platforms like Lendesca.com that help buyers evaluate total acquisition costs can assist in benchmarking this ratio against comparable funeral home transactions in your market. Pair this with a comprehensive insurance coverage audit to understand the full risk transfer picture.

Red Flags

- Multiple claims from the same department or role — suggests a systemic safety failure, not bad luck

- No documented safety program — NFDA safety resources outline industry standards that should be in place

- High employee turnover correlating with claims — new employees are disproportionately likely to be injured, and turnover creates a cycle of inexperienced workers handling dangerous tasks

- EMR above 1.25 — anything at this level warrants a serious pricing conversation

- Workers’ comp audit adjustments — if the insurer has adjusted premiums after audit, it means payroll was misreported, which raises broader accuracy concerns about the seller’s financial disclosures

Structuring the Deal Around Workers’ Comp Risk

Workers’ comp cost is not fixed. It is a variable you can negotiate around, plan for, and improve over time. Here is how to incorporate it into your deal structure.

High EMR = Price Reduction

A high EMR has a quantifiable, multi-year impact on operating costs. Calculate the premium difference between the current EMR and a 1.0 EMR, then project that difference over three years (the time it takes for inherited claims to roll off the calculation). That number is your negotiating basis for a purchase price reduction.

Example: A funeral home pays $35,000 per year in workers’ comp premium with a 1.30 EMR. At 1.0, the premium would be approximately $27,000. The $8,000 annual difference over three years is $24,000 in excess cost you are inheriting. That is a legitimate basis for a $20,000–$25,000 price reduction.

Require Settlement of Open Claims

Open claims with large reserves are dragging the EMR up and creating uncertainty about future costs. Make it a condition of closing that the seller resolve open claims to the extent possible — either through settlement, return-to-work programs, or insurer negotiation to reduce reserves.

Consider Entity Structure Carefully

If your state allows it and the deal is structured as an asset purchase, establishing a new entity with a new FEIN may result in a 1.0 starting EMR. But consult your insurance broker and your state’s rating bureau rules before relying on this strategy. As discussed above, combination rules can transfer the prior EMR to your new entity if the operations continue without material change.

Your staffing continuity plan should account for how entity structure decisions affect both workers’ comp and employee retention.

Post-Acquisition: Driving EMR Below 1.0

Once you own the funeral home, you control the safety culture. A focused effort can bring the EMR below 1.0 within three years:

- Implement a formal safety program — written policies for lifting procedures, chemical handling, PPE requirements, and vehicle operation

- Invest in equipment — hydraulic lifting tables in the prep room, powered gurney systems for removals, proper ventilation upgrades

- Train relentlessly — new employee orientation with safety emphasis, quarterly refreshers, documented training records

- Report and investigate every incident — even near-misses, because the data reveals patterns before they become claims

- Manage claims aggressively — return-to-work programs, regular communication with the insurer, prompt reporting

A funeral home that moves from a 1.30 EMR to a 0.80 EMR saves 50 percentage points on its annual premium. On a $35,000 base premium, that is $17,500 per year in savings — $52,500 over three years. Those savings flow directly to the bottom line and increase the resale value of the business.

Insurance Broker Selection

Not all insurance brokers understand funeral homes. The classification codes, the risk profile, the EMR nuances, and the coverage gaps specific to funeral service require a broker with industry experience.

Ask prospective brokers:

- How many funeral homes do you insure?

- Do you have relationships with carriers that specialize in funeral service?

- Can you provide EMR projections based on different safety program investments?

- Do you offer loss control services tailored to funeral home operations?

The right broker will save you more in premium optimization than they cost in commissions. The wrong broker will put you in a generic small-business program that misprices your risk and leaves coverage gaps.

Frequently Asked Questions

Can I shop for a new workers’ comp policy immediately after closing?

You can and should get competitive quotes, but your EMR follows you to every carrier. Switching insurers does not change your EMR. What it can change is the base rate, the carrier’s underwriting appetite for funeral homes, and the quality of claims management — all of which affect your total cost.

What if the seller did not carry workers’ comp?

In most states, workers’ comp is mandatory for businesses with employees. A funeral home operating without coverage has been operating illegally, and you inherit the exposure for any injuries that occurred during that period. This is a serious red flag that should be investigated thoroughly before proceeding. It also likely correlates with worker misclassification issues — sellers who skip workers’ comp often classify employees as 1099 contractors to avoid the requirement.

How quickly can I improve the EMR?

The EMR calculation uses a three-year window. If you have zero claims in your first year of ownership, the worst year in the historical window will begin to roll off after the first recalculation. Most owners see meaningful improvement within 18–24 months and can reach a sub-1.0 EMR within three years if they invest in safety programs and claims management.

Does the EMR affect anything besides workers’ comp premium?

Yes. General contractors and government agencies often require subcontractors and vendors to maintain an EMR below 1.0 or 1.25. If the funeral home does any contract work (such as providing removal services to a county coroner’s office or a hospital system), a high EMR can disqualify the business from those contracts. Some commercial landlords also review EMR as part of lease negotiations.

The Bottom Line

Workers’ compensation is not a line item you can ignore until renewal time. In a funeral home acquisition, the EMR is a direct, quantifiable variable that affects your operating costs for at least three years after closing. A high EMR is a negotiating tool — use it to reduce the purchase price. A low EMR is a competitive advantage — protect it with investment in safety and claims management.

Pull the loss runs. Calculate the EMR impact. Benchmark the premium against revenue. Then structure the deal accordingly. The funeral home’s claims history tells you something important about how the business has been managed — and what it will cost you to manage it better.

This guide is part of the Funeral Home Buyer resource library — acquisition intelligence for serious buyers, from due diligence through operations.

Funeral Home Buyer provides educational content for professionals evaluating business acquisitions in the funeral services industry. This article is not legal, financial, or investment advice. Consult qualified professionals before making acquisition decisions.