Most of the content written about buying a funeral home describes a business that doesn’t exist in half the counties in America. The models assume 200-plus annual calls. Multiple arrangement rooms. A staff of five or more. An EBITDA that justifies a 3×–5× multiple. A market where competitors are measurable in drive-time radius.

That is not what you are looking at.

You are looking at a funeral home in a town of 4,000 people. Eighty-five calls a year. One prep room, one chapel, one visitation room that doubles as overflow. The owner is 72, has no succession plan, and has been the only funeral director in the county for three decades. The asking price is $350,000 — building included.

This is a real deal. They are everywhere. And they play by completely different rules than anything the metro-focused acquisition playbooks prepare you for.

What ‘Rural’ Actually Means in Funeral Home Economics

There is no official definition, but for acquisition purposes, “rural” means a funeral home where the economics are shaped primarily by geographic isolation and small population. In practice, that looks like this:

- Service area population under 15,000. Often significantly under. The town itself may be 2,000–5,000 people, with the service area extending across the surrounding county and sometimes into adjacent counties.

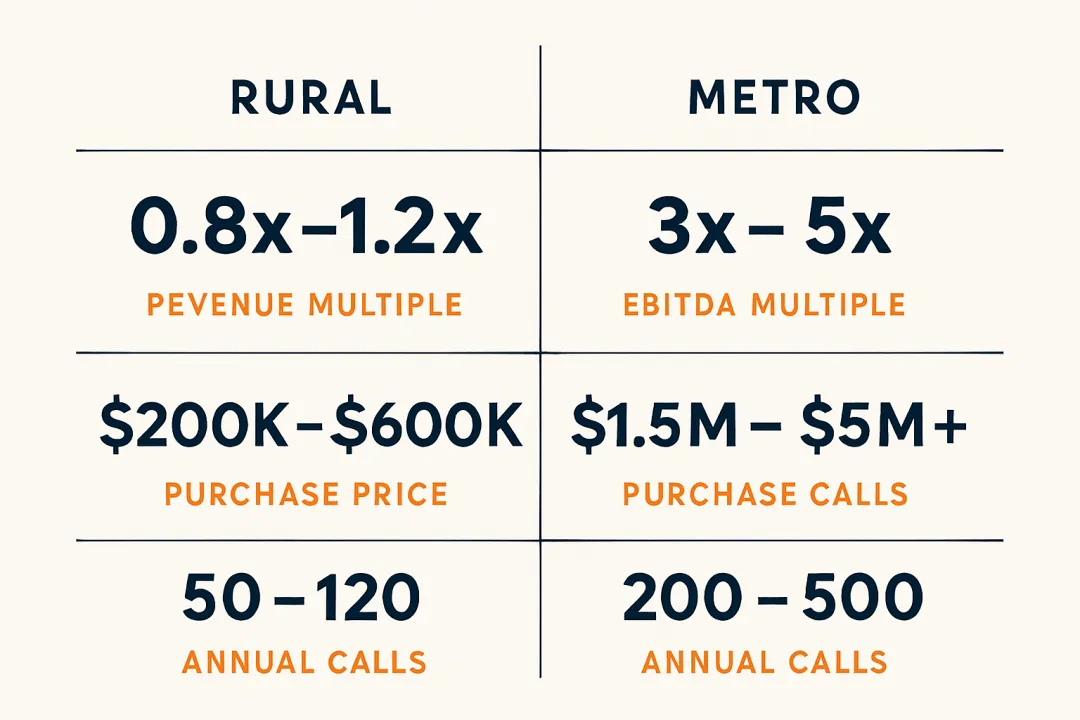

- Annual call volume under 150. Many sit in the 50–120 range. Some handle fewer than 75 calls a year. The national average for independent funeral homes is roughly 113 calls annually — rural operations skew well below that.

- One funeral home, or one of two, in the county. In metro markets you compete on service quality, branding, facilities. In a rural market, geography does most of the work. Families use the funeral home that is closest. Period.

- Owner-operated. The funeral director is the owner, the embalmer, the driver, the person answering the phone at 3 a.m. There may be one part-time assistant or a spouse who handles bookwork. That is the entire operation.

The revenue picture

A rural funeral home handling 85 calls at an average revenue per call of $7,500 generates roughly $637,500 in annual revenue. At 120 calls, you are looking at $900,000. At 50 calls, $375,000.

These numbers make metro-market buyers blink. But the cost structure is proportionally different. There is no $15,000/month facility lease. No payroll for five full-time employees. No marketing budget. The owner’s discretionary earnings on $637,500 in revenue can easily reach $150,000–$200,000 when you account for the fact that the owner is doing everything, the building is owned free and clear, and overhead is minimal.

Why private equity skips these

Service Corporation International, Park Lawn, Foundation Partners, Everstory — none of them are buying a funeral home that does 85 calls a year in a county with a declining population. The economics don’t justify the transaction costs. Legal fees, due diligence, integration overhead, and management infrastructure cost roughly the same whether you are acquiring a $400,000 operation or a $4 million one. At sub-$1 million revenue, the math doesn’t pencil for institutional buyers.

This is an advantage for you. These deals sit in a zone that is too small for corporate acquirers and too niche for generalist business brokers. Many never appear on any marketplace. The seller tells their attorney, their CPA, or a colleague at the state funeral directors’ association that they are thinking about retiring. That is the listing.

Who these deals are actually for

Rural funeral home acquisitions work for a specific buyer profile:

- Someone willing to live in or near the community. This is not an absentee-ownership play. Rural funeral service is personal. The community needs to know you, trust you, and be able to reach you. You will be at Rotary meetings, high school football games, and church suppers. That is not optional — it is the business model.

- A buyer who wants a living, not an empire. Eighty-five calls a year, $150,000–$200,000 in owner’s discretionary earnings, minimal debt service, and a pace of life that metro acquirers can’t imagine. If that sounds like enough, keep reading.

- An investor building a small rural portfolio. Two or three rural locations within an hour’s drive of each other, sharing staff and resources. This is the one scalable model in small markets, and it works.

The Hidden Advantages of Small-Market Deals

The risks of rural acquisition get plenty of attention. The advantages don’t. Here is what the metropolitan-focused acquisition content consistently misses.

Zero or minimal competition

In metro markets, a family choosing a funeral home has options within a 15-minute drive. In a rural market, the nearest competitor may be 30, 40, or 50 miles away. That distance is the strongest competitive moat in the industry.

When you are the only funeral home within 30 miles, your market share is not 25% or 40%. It is 80% to 95%. Families in grief do not drive an hour to save $500. They use the funeral home that is close, familiar, and available. As long as you provide competent, respectful service, that referral pattern does not change.

Community loyalty runs deep

A rural funeral home that has served a community for decades has something no metro competitor can replicate: institutional memory. The funeral director who buried your grandfather also buried your father. That relationship is not a line item on a balance sheet, but it functions like recurring revenue.

This loyalty transfers to a new owner — not automatically, but reliably — if you handle the transition correctly. The previous owner introduces you. You show up to community events. You learn names. Within 18–24 months, the community treats you like their funeral director. In metro markets, that kind of loyalty takes a generation to build. In small towns, it transfers with the business if you earn it.

Lower entry cost

Purchase prices for rural funeral homes, including real estate, typically range from $200,000 to $600,000. Many fall in the $250,000–$450,000 range. Compare that to metro-area funeral homes where $1.5 million to $3 million is the starting point and $5 million-plus is common for established operations.

The lower entry cost means:

- Smaller down payments. An SBA 7(a) loan on a $400,000 acquisition requires roughly $40,000–$60,000 down, depending on your lender and the deal structure. That is accessible capital for most mid-career professionals.

- Lower debt service. Monthly loan payments on $350,000 are manageable against $150,000+ in annual owner’s earnings. The debt service coverage ratio on these deals is often better than metro acquisitions because the purchase price is proportionally lower relative to earnings.

- Less catastrophic downside. If the deal doesn’t work out, you are unwinding a $400,000 transaction, not a $3 million one. The real estate alone provides a floor on your exposure.

Simpler operations

A rural funeral home is operationally straightforward compared to a large metro operation. No complex staffing schedules. No fleet of ten vehicles. No competing with corporate operators on facilities and technology. You are managing a small, high-touch service business. If you have run any small business — or managed a P&L of any kind — you can learn the operational layer.

The regulatory requirements are the same everywhere: state licensing, FTC compliance, OSHA standards, environmental regulations. But the operational complexity of executing against those requirements in an 85-call operation is dramatically lower than in a 400-call metro firm.

The multi-location rural model works

Impact Funeral Partners and a handful of smaller operators have built strategies specifically around acquiring small-town funeral homes. The model: buy two, three, or four rural locations within a 60–90 minute driving radius. Share staff, share vehicles, share back-office functions. Each location maintains its own identity and community presence. The central owner manages across locations.

This model turns the “it’s just a job” criticism of single-location rural ownership into something with genuine scale economics. Three 80-call locations become a 240-call operation with a single management layer and shared overhead. That is a business with real enterprise value.

The Real Risks You Need to Understand

Rural funeral homes have real structural risks that don’t exist — or exist differently — in metro markets. Every one of these is manageable, but none should be dismissed.

Population decline

This is the existential risk. Many rural counties in the United States are losing population. Young people leave for cities and don’t come back. The remaining population skews older, which temporarily increases death rates — but that cohort is finite. A county that has 12,000 residents today and 9,500 in ten years will generate fewer calls, not more.

Before you sign anything, pull the data:

- Census Bureau population estimates for the county and surrounding counties, 2010 to present. You want trend lines, not a single snapshot.

- State demographic projections. Most state demographers publish county-level population projections 10–20 years out.

- School enrollment data. Declining school enrollment is a leading indicator of long-term population loss.

- Economic anchors. Is there a hospital, a manufacturing plant, a military base, a university? Communities with an institutional anchor tend to stabilize. Communities whose economy was a single employer that left do not recover.

Not every rural county is declining. Some are stable. A few — particularly those within 60–90 minutes of a growing metro area, or those with lifestyle appeal (retirement destinations, outdoor recreation hubs) — are growing. The population story varies enormously. Do the homework.

Staffing isolation

In a metro market, you can recruit a licensed funeral director from the applicant pool within 50 miles. In a rural market, there may not be a licensed funeral director available within 100 miles who is not already employed. This challenge is part of the broader staffing crisis in funeral services.

This has several implications:

- You may need to get licensed yourself. If you are the owner and sole funeral director, your ability to take a vacation, get sick, or attend your own family emergencies depends on having backup. Many rural owners get licensed specifically for this reason, even if they didn’t enter the industry from a mortuary science background.

- Contract embalmers cover the gap. A contract embalmer who serves multiple rural funeral homes within a region can be your flex capacity. Build this relationship before you need it.

- Retention is everything. If you have a good employee — a part-time assistant, a removal technician, an apprentice — do whatever it takes to keep them. The replacement pipeline doesn’t exist the way it does in metro markets.

The 24/7 on-call reality

An 85-call-a-year funeral home averages roughly 1.6 calls per week. That sounds manageable. But deaths don’t follow a schedule. You may go ten days with nothing, then get three calls in 48 hours. Every one of those calls requires an immediate response — a removal from a hospital, a nursing home, or a private residence, at any hour.

In a metro operation, on-call rotation spreads this across multiple staff. In a sole-proprietor rural operation, on-call is you. Every night. Every weekend. Every holiday.

This is the single most common reason rural funeral home owners burn out and the single most common surprise for new buyers. Before you commit, spend a week shadowing the current owner. See what 3 a.m. removal calls feel like. Understand what you are signing up for.

Facility condition

Rural funeral homes are often in buildings that are 50–80 years old. Deferred maintenance is the rule, not the exception. An owner who has been operating for 30 years and planned to “sell when I retire” frequently stopped investing in the building a decade ago.

What to inspect:

- Roof, HVAC, plumbing, electrical. Get professional inspections on all four. Budget $30,000–$75,000 for deferred maintenance on a typical rural funeral home. Some will need more.

- ADA compliance. Many older rural funeral homes are not ADA compliant. Ramps, doorways, restroom access — these are not optional, and they can be expensive to retrofit in historic buildings.

- Environmental concerns. Older prep rooms may have formaldehyde ventilation issues. Underground storage tanks from previous heating systems. Asbestos in floor tiles or insulation. An environmental Phase I assessment costs $2,000–$4,000 and is worth every dollar.

- Cosmetic condition. A dated funeral home signals neglect to families. Budget for cosmetic updates in your first year — carpet, paint, lighting, landscaping. These are high-return investments in a business built on first impressions.

Cremation pressure without volume

The national cremation rate has surpassed 60% and continues to climb. In rural markets, cremation adoption historically lagged metro areas but is catching up. The challenge: a rural funeral home rarely has the volume to justify owning its own crematory (retort). A retort costs $150,000–$300,000 to install and requires consistent volume to operate efficiently.

Most rural operators outsource cremation to a regional crematory, paying $250–$500 per cremation. That outsource cost eats into your margin on cremation cases, which already generate lower revenue than traditional burial services. At 85 calls a year with 50% cremation, you are outsourcing roughly 42 cremations annually at a cost of $10,500–$21,000.

This is manageable, but it means cremation-heavy years compress your margins. Track the cremation rate trend in your market. If it is climbing faster than your ability to offset through pricing, that is a slow-moving squeeze.

Valuation: Why the Math Is Completely Different

Walk into a metro funeral home valuation conversation and you will hear “3× to 5× EBITDA” within the first five minutes. Walk into a rural valuation and that framework falls apart.

Revenue multiples, not EBITDA multiples

At sub-$1 million revenue, EBITDA-based valuation is unreliable because owner compensation distorts the number. A sole proprietor paying themselves $130,000 from $600,000 in revenue has a very different EBITDA than one paying themselves $80,000 — and neither number reflects what a new owner’s actual earnings would be.

Rural funeral homes typically trade on revenue multiples:

- 0.8× to 1.2× annual revenue for the business operations (goodwill, customer relationships, trade name, rolling stock, equipment).

- Plus fair market value of real estate, if included. In rural markets, the real estate is often worth $75,000–$200,000 — sometimes more than the business itself.

- Total transaction value of $200,000–$600,000 for a typical rural acquisition, with outliers on both sides.

Compare that to metro funeral home valuations of 3×–5× EBITDA, which translates to 1.5×–3× revenue on a typical operation. The rural discount exists because of scale, risk, and buyer pool size.

Book value matters more

At these price points, the tangible asset value of the business — the real estate, the vehicles, the preparation equipment, the casket inventory — represents a meaningful percentage of the purchase price. In a $400,000 deal, the real estate might be worth $150,000 and the equipment and vehicles another $75,000. That is $225,000 in hard assets against a $400,000 purchase price.

This asset floor limits your downside. Even if the business fails entirely, you own a commercial building and specialized equipment with liquidation value. Metro acquisitions at 4× EBITDA have no such floor — you are paying almost entirely for goodwill.

The ‘job value’ question

Here is the honest assessment that most brokers won’t lead with: a rural funeral home doing 85 calls a year is a good job, not a scalable business. The owner’s discretionary earnings of $150,000–$200,000 include compensation for that owner doing all the work. If you hire a managing funeral director at $65,000–$85,000 to replace yourself, your “return on investment” drops dramatically.

This is not a reason to avoid the deal. It is a reason to price it correctly and enter it with the right expectations. You are buying a livelihood, a lifestyle, and a community role. If you price it as a financial investment and expect passive returns, you will be disappointed.

Single-location rural funeral homes are valued as practitioner businesses, not as investment-grade enterprises. That changes when you aggregate multiple locations — but for a single operation, be honest about what you are buying.

Seller expectations can be misaligned

A seller who has run the funeral home for 35 years often values the business based on community standing, not financial performance. “Everyone in town knows my name” is real, but it’s not worth $200,000 in goodwill above and beyond the financial fundamentals.

You will encounter sellers who believe their business is worth $700,000 because they heard a metro funeral home sold for 3× revenue. It’s your job — or your broker’s or attorney’s job — to respectfully explain why their 85-call rural operation is not comparable to a 300-call suburban firm.

Have the data ready. DealStream, BizBuySell, and funeral home brokerage firms like NewBridge Group publish transaction data and comparable sales. State funeral directors’ associations sometimes have valuation resources. Come to the conversation with recent comparable rural transactions, not metro benchmarks.

Due Diligence Adjustments for Rural Acquisitions

Standard funeral home due diligence applies to rural deals. But several items deserve heightened scrutiny.

Service area analysis

This is the most important piece of rural due diligence and the one most buyers rush through. You need to understand:

- Population trends. County-level, 10-year historical and 10-year projected. Adjacent counties, too — you pull calls from them.

- Age demographics. What percentage of the population is over 65? Over 75? This tells you about near-term call volume potential and medium-term decline risk.

- Competitor mapping. Identify every funeral home within a 45-mile radius. Mark drive times, not mileage. A funeral home 30 miles away across a mountain pass is less competitive than one 20 miles away on an interstate.

- New entrants. Is anyone building? Has anyone applied for an establishment license in the service area? Your state funeral board can provide this.

- Cremation-only providers. Direct cremation providers operating remotely can undercut your cremation pricing without a physical presence in your market.

Facility assessment

Budget for a detailed building inspection by someone who understands commercial properties, not just residential home inspectors. Specifically:

- Structural integrity of the building, particularly if it was originally constructed as a residence and converted

- Prep room ventilation and plumbing (OSHA compliance)

- Underground storage tanks

- Asbestos, lead paint in pre-1978 buildings

- Septic systems (many rural funeral homes are not on municipal sewer)

- Well water systems, if applicable

- Parking adequacy for services (local zoning requirements vary)

Preneed book review

Preneed contracts — funeral arrangements paid in advance — are both an asset and a liability. In rural markets, the preneed book can represent a meaningful percentage of future revenue. Review the following:

- Total number of funded preneed contracts. How many families have already paid for future services?

- Funding mechanism. Are contracts funded through insurance assignments or trust accounts? Insurance-funded contracts are generally cleaner for buyers.

- Trust compliance. If trust-funded, are the trusts in compliance with state regulations? Are the funds actually there? This requires an independent audit, not a review of the seller’s records.

- Pricing guarantees. Do the contracts guarantee a specific service at the price paid, or are they priced at the time of need? Guaranteed-price contracts funded ten years ago at $4,000 for a service that now costs $7,500 are a loss on every one.

- Assignability. Can the preneed contracts transfer to a new owner? In most states, yes, but the mechanics vary.

Community relationships

In rural markets, relationships are infrastructure. Map them:

- Hospice organizations serving the area. Who calls whom when a patient passes? Is there a standing relationship? Understanding this referral ecosystem is critical.

- Hospitals and nursing homes. Who has first-call agreements? Some facilities rotate between funeral homes; others have informal preferences.

- Clergy. In many rural communities, the relationship between funeral director and local clergy is deeply established. Meet the pastors, priests, and rabbis before you close. Their endorsement matters.

- County coroner or medical examiner. Rural coroners are often elected officials, not medical professionals. Understand the working relationship.

- Veterans’ organizations. In communities with a strong veteran population, military honors and veteran-specific services are significant. The VFW or American Legion honor guard may have a longstanding relationship with the funeral home.

Licensing variations

State licensing requirements for funeral establishment transfers vary. Some states require a new establishment license when ownership changes. Some require only a name change filing. A few require the new owner to meet specific experience or education requirements.

Do not assume your attorney or the seller’s attorney knows funeral-specific licensing rules. Hire an attorney who has handled funeral home transactions in that specific state, or retain a specialized consultant. The state funeral board is your primary resource, but their interpretations can vary by examiner.

Making It Work: Operational Strategies for Small-Market Owners

You’ve found the deal. The valuation works. Due diligence is clean. Now you need to operate profitably in a market that doesn’t offer the margin of error a metro market does. Here is what works.

The multi-location rural model

If you are serious about building something beyond a single practitioner operation, this is the path. Acquire two or three rural funeral homes within a 60–90 minute drive of each other. Each location keeps its name, its community identity, and its local presence. Behind the scenes, you share everything possible.

How it works in practice:

- Shared staffing. One licensed funeral director can serve as a float across locations. When location A has a service, the director drives there. When location B needs prep work, same director. You maintain one part-time local presence at each location for first-call response and community face.

- Shared vehicles. Instead of each location owning a hearse, a removal vehicle, and a flower car, you maintain a smaller combined fleet that rotates.

- Centralized back office. One bookkeeper, one accounting system, one preneed administration process. The per-location cost of administration drops with each acquisition.

- Combined purchasing power. Casket suppliers, vault companies, and merchandise vendors offer better pricing at 200+ units than at 80.

Three 80-call locations become a 240-call operation with aggregate revenue of $1.8 million. That is a business worth building — and one that has genuine enterprise value if you ever want to sell.

Shared services and outsourcing

For a single-location operator, shared services are survival strategy:

- Contract embalming. A regional contract embalmer who serves multiple rural funeral homes costs $250–$400 per case. At 85 calls with perhaps 40–50 requiring embalming, that is $10,000–$20,000 annually. Less than half the cost of a full-time employee.

- Outsourced cremation. Partner with the nearest crematory. Negotiate a volume rate if possible. Build redundancy — know two crematories you can use, in case one has equipment downtime.

- Shared livery. In some regions, funeral homes share hearse and limousine services for large funerals. This is more common than outsiders realize.

- IT and technology. Cloud-based funeral management software (Passare, Halcyon, FuneralOne) runs the same at 85 calls as at 500. The per-unit cost is higher, but the functionality is identical. Online arrangement conferences, digital general price lists, and tribute websites are not metro luxuries — they are expected everywhere now.

Community integration

This is not a nice-to-have. In a rural market, community integration is the entire competitive strategy.

Within your first 90 days:

- Join the Rotary Club, Lions Club, or whatever civic organization is active in town

- Introduce yourself to every clergy member within 20 miles

- Meet the hospice coordinator, the hospital administrator, and the nursing home director

- Sponsor a Little League team, a 4-H event, or the county fair

- Show up at the diner where everyone eats breakfast

Within your first year:

- Offer a free annual community grief seminar or memorial event

- Partner with hospice on bereavement support

- Host a veterans’ memorial event on Memorial Day or Veterans Day

- Make your chapel available for community events when not in use for services

None of this is altruistic (though it can be personally rewarding). It is the marketing strategy. In a rural market, your reputation is your brand. Every community interaction is a marketing impression. The funeral director who coaches youth basketball is the funeral director families call when grandma passes.

Technology leverage

Technology doesn’t replace community presence, but it extends your reach:

- Online arrangements. Families increasingly expect the option to begin arrangements online or via video call, even in rural markets. This is especially important for out-of-town family members who can’t drive three hours to meet in person.

- Digital preneed. Offer preneed planning through your website. Rural demographics skew older, but their children — who are often making or influencing the decision — are digitally fluent.

- Social media presence. A simple, consistent Facebook presence matters more in a small town than a polished website. Post obituaries, share community events, mark milestones. In many rural communities, the funeral home’s Facebook page is the primary obituary source.

- GPS-enabled removal tracking. When families call at 2 a.m., being able to tell them “I’m 15 minutes out” via a simple text provides reassurance that a phone tree cannot.

The lifestyle calculation

Here is the final, honest assessment. A rural funeral home at 85 calls a year generates $150,000–$200,000 in owner’s discretionary earnings with minimal debt service on a $350,000 acquisition. You work hard during busy stretches and have genuine downtime during slow ones. You are always on call but not always busy. You live in a community where your mortgage or rent is a fraction of metro costs, where your children attend schools where teachers know their names, and where your professional identity carries real social weight.

The trade-off: you live in a small town. Your dating pool, restaurant options, and cultural amenities are limited. The nearest major airport may be two hours away. Your children may leave for college and not come back, just like the children of the families you serve.

For some buyers, that trade-off is the entire point. They are leaving a metro career precisely because they want a slower pace, a tighter community, and a business that matters to the people around them. For those buyers, a rural funeral home is not a consolation prize — it is the goal.

For others, the isolation becomes corrosive within two years. Know yourself before you commit.

Frequently Asked Questions

How do I find rural funeral homes for sale?

Most are not publicly listed. Start with your state funeral directors’ association, which often maintains an informal network of owners considering retirement. NewBridge Group and The Foresight Companies occasionally list rural properties. Direct outreach — a respectful letter to an aging owner expressing interest — is the single most productive sourcing method for these deals.

Can I get SBA financing for a rural funeral home?

Yes. SBA 7(a) loans are commonly used for funeral home acquisitions, including rural ones. The SBA does not discriminate by market size. However, your lender may scrutinize population trends more carefully and require a larger down payment if the demographic outlook is unfavorable. Live Oak Bank and Ready Capital are among the lenders with specific funeral home lending experience.

What if the owner wants to stay on for a transition period?

This is common and usually beneficial in rural deals. A 6–12 month transition where the seller introduces you to the community, trains you on local customs and relationships, and handles calls alongside you is worth negotiating. Structure it as a consulting agreement with clear terms, a defined end date, and non-compete provisions.

Do I need a funeral director’s license to own a rural funeral home?

In most states, no. You need a licensed funeral director on staff (or yourself, if you obtain the license), but ownership does not require personal licensure in the majority of states. However, in a sole-proprietor rural operation, getting licensed yourself dramatically simplifies staffing and on-call coverage. Many rural owner-operators pursue licensure even if they didn’t enter the industry from a non-industry background.

Is remote or absentee ownership viable for rural funeral homes?

Rarely. Rural funeral service depends on personal presence and community trust in a way that metro operations do not. An absentee owner of a rural funeral home is paying a managing funeral director’s salary out of a revenue base that barely supports one owner’s compensation. The math is difficult and the community perception risk is high. If you are not willing to relocate to the area, a rural acquisition is probably not the right fit.

Rural funeral homes are the overlooked middle of the acquisition market. Too small for institutional capital. Too niche for generalist brokers. Too far from metro areas for most buyers to consider. That’s exactly what makes them opportunity — if you are the right buyer, with the right expectations, willing to do the work of becoming part of a community that needs what you are offering.

The deals are there. The question is whether you are.

This guide is part of the Funeral Home Buyer resource library — acquisition intelligence for serious buyers, from due diligence through operations.

Funeral Home Buyer provides educational content for professionals evaluating business acquisitions in the funeral services industry. This article is not legal, financial, or investment advice. Consult qualified professionals before making acquisition decisions.